Clarise vs. the Accountant

Financial Analysis

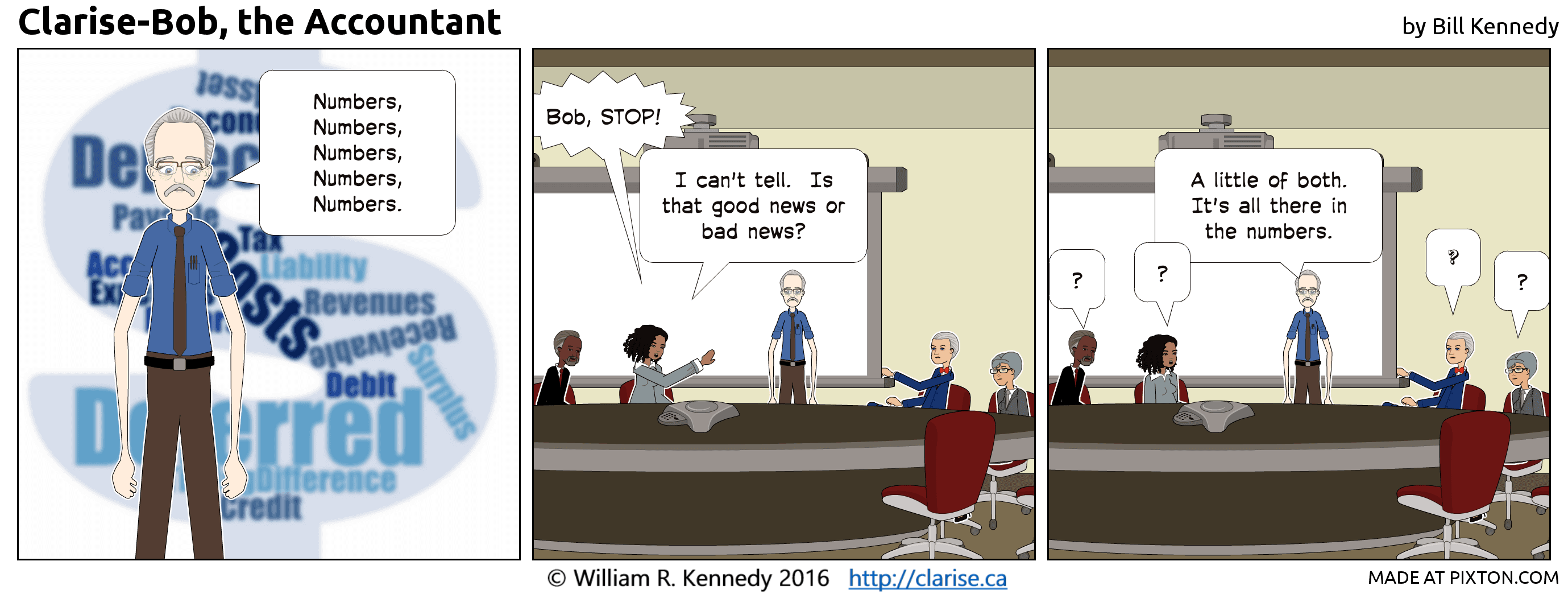

Have you ever read an accounting analysis that sounded something like this:

The negative variance this month is due in part to budgetary timing differences offset by expense accruals . . .

Is that news good or bad? Who knows? What’s clear is that accounting jargon is distorting the message. Now, most analysis doesn’t get quite this bad, but jargon is a big issue in financial statement analysis. Here’s a little primer:

Variance – the difference between two numbers, e.g. this year and last year or this year and budget. A positive variance is good. A negative variance is bad.

Timing Difference – typically means that an expense was expected but it occurred in a different month (either earlier or later) than originally forecast. This is neither good nor bad news. It just explains why the number is different.

Accruals – see below for a more detailed description. Accruals mean you recognize your income when you earn it, not when the money comes in and you record your expense when you owe the money or have used the good/service, not when the money is actually paid.

For me the biggest issue with financial analysis is not the jargon, however, it’s the tendency to say what happened, but not why. Decision makers need to know things are going right (or wrong) in order to make good decisions. Knowing that an expense went over budget is only half the battle. You need to know why as well.

Accruals

I first was promoted to Controller during a shakeout at an insurance brokerage which went right to the top. After a couple of months, the new president called me into his office to explain why “my” sales number was different than his. He was trying to understand the financial statements and he had copied all of the invoices issued to customers in the month. I explained that some of our policies went for more than one year and we had to wait until we earned the commission in the future years before we could include the money in our sales numbers. It made sense to him. It also helped de-mystify the whole accounting process for him.

But I think the final word has to go to the Vice-President who cured me of my accounting financial analysis jargon. He said to me, “Bill, from now on I want to see the words, ‘Good News’, or ‘Bad News’ at the top of your analysis reports.”

That’s what it all comes down to, isn’t it?

Leave a Reply